Keep em Guessing, Let em Worry

We want to see more jobs. We want to see lower unemployment. We want to see a stronger economy that can cause the improvement to be sustained.

Ben Bernanke, September 2012

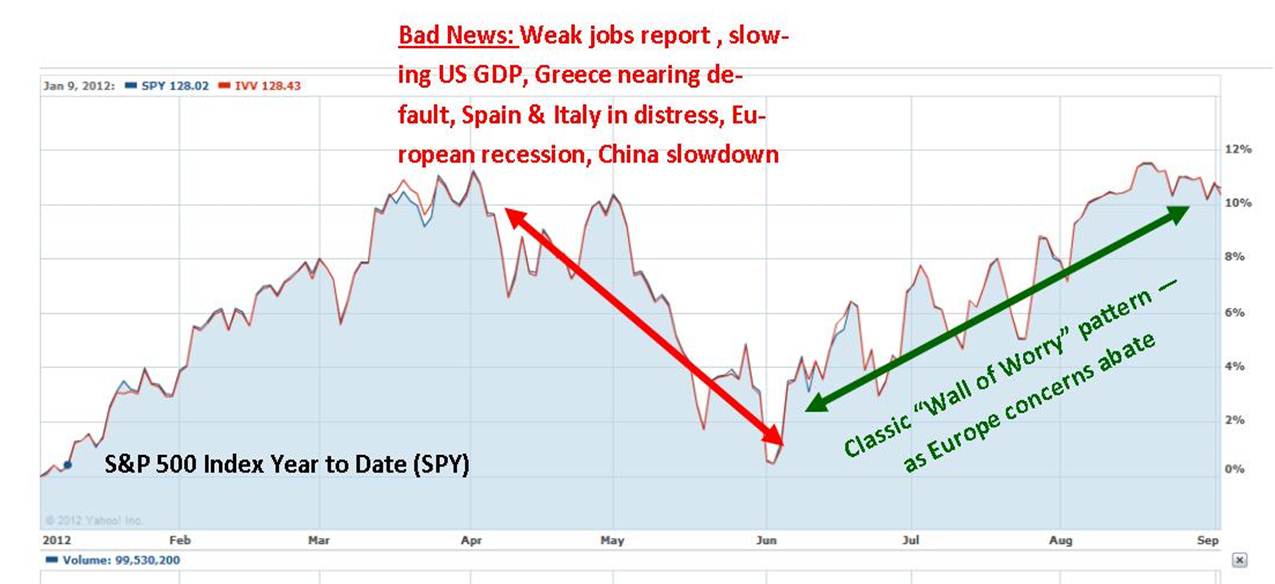

Huge economic problems in Greece, Spain, Italy and France? Heard it. Chinas economy slowing? Been there. A US unemployment rate over 8%? Yawn. Equity markets up over 10% for the year? So what. What Fiscal Cliff? The narrative of the jaded investor and the markets continues despite all the day-to-day sturm und drang that dogs the headlines. Are investors so numbed by the consistent parade of scares since August 2007 that anything short of sudden and terrifying crisis can get their attention? Or, is the slow but still significant improvement in the economy since 2009 sufficiently real to justify quiet optimism and hope?

We think its a combination of both. Moderate non-drug-induced desensitization mightnt be such a bad idea after nearly four years of near-hysteria. And above all else, one important fact is clear: despite the glacial pace of improvement, the economy is far better off today than just 3 years ago and after having weathered a near-miss economic Armageddon that kicked off the Great Recession a few short years ago.

Perhaps most importantly, Eurozone issues, China, and problems in the US are, frankly, old news. Unlike a year ago, the risks and possible impacts are known, and that is critically important. Fear of the unknown, after all, is what creates financial nightmares. Its likely that the markets feel that they have a grasp, albeit uncertain, of the problems and solutions, painful and complex though they are.

Major, very real challenges remain, frankly, not the least of which is that a sizeable chunk of Congress seems comfortable with committing economic hari-kari. Well see if those just to the right of Gunga Din are willing to put down their clubs and spare the US another government shutdown and S&P credit downgrade, and give up the goal of proving that government doesnt work after effectively destroying it. Should the Republicans take both houses and the Presidency, we can expect further painful cuts to social services and government jobs, which could push the economy back into recession. Thats not a likely outcome, however.

With those caveats in mind, short of a massive government effort to stimulate high quality jobs and critical industries, we expect the lackluster economy to continue to stumble forward, until such time as the natural business cycle picks up momentum and makes the recovery more obvious to all. The markets should continue to anticipate this slow, largely positive trend, and continue to benefit. A major geopolitical event or another domestic crisis could quickly very quickly derail this three-wheeled, precariously balanced train. But we feel that the derailment would still largely be temporary.

Dear Investor

Will he? Wont he? He will! The wait, finally, after months of conjecture as to whether or not Ben Bernanke would instigate a new round of Federal Reserve actions that might attempt to stimulate the economy, is over. After months of having danced around on the issue of whether the economy is sufficiently impaired to attempt to inject more stimulus through quantitative easing, or not, and implying by inaction that the economy isnt all that bad, the verdict is in. For months, Mr. Bernanke masterfully kept everyone in limbo, all along imploring Congress, with an increasingly louder voice, to take action to provide needed stimulus. The Congress remained steadfastly tin-eared, however, with the Fiscal Cliff, the legislation passed by the Congress that mandates broad, radical, and deep cuts across the board to key programs and defense expenditures alike at the end of 2012 (discussed shortly). Bernanke, recognizing the crushing impact this is likely to have on the economy, said enough is enough, and moved strongly.

Even though on first blush, the new, third round of stimulus, called QEIII (Quantitative Easing) seems modest at best in terms of impact, the words and commitment that are accompanying this effort border on extraordinary. Steering away from the usual focus on inflation, Bernanke appears willing to wage war against joblessness and for economic growth.

QEIII hits on several levels. First, recognizing the importance of stimulating housing and through it, employment, the Federal Reserve will seek to purchase weaker mortgage backed securities from banks to help them clean up their balance sheets, freeing them to offer up new and lower rate mortgages. Second, the Fed will extend near-zero short term interest rate lending to banks through 2015. Third, the Fed will continue to monitor and is prepared to act on job data for the indefinite future as it has elevated its focus on jobs and employment.

While many economists and Congressional Republicans criticized the action as likely having little or no impact, they and most of the media and their collective talking points are missing the real point: this is Bernankes shot across the bow of a dysfunctional Congress, basically telling the Radical Right if you wont take action to stimulate the economy and jobs, I will. The Fed gave clear direction that it would continue, on a monthly basis, to consider job growth and take what it feels to be appropriate actions to help improve the situation. Bernanke has effectively thrown down the gauntlet.

The weak job market should concern every American The idea is to quicken the recovery, to help the economy begin to grow quickly enough to generate new jobs. Ben Bernanke, 9/13/2012

Frankly, Congress inaction forced Mr. Bernankes hand. With the Federal Reserve having the dual mandate of both keeping inflation under control and helping to achieve full employment, and with Congress paralysis on the latter, the Fed Chairman, despite a lack of consensus on the Federal Reserve Board (until recently, at least), felt it necessary to attempt to step on the gas to encourage additional lending.

Jobs, jobs, jobs. What has Mr. Bernanke distressed about is quite clear. Unemployment continues to be painfully high, with over 20 million people unable to secure full time employment, and economic growth excruciatingly low, at an abysmal 1.5% this past quarter. The European recession has further weakened the economy both abroad and at home, and Chinas economy, which like the rest of the world is still reeling after the great financial crisis, is growing more slowly than expected. The upshot is that economic growth, rather than the already low post-recession 3% range experienced much of last year, is now crawling along at half that. The economy is simply not producing jobs at the rate expected and needed, as Mr. Romney is quick to point out.

A rally scorned. So amid this extreme wall of worry, the equity markets, believe it or not, have rallied nearly 12% this year. This hated rally, so called because of the level of fear and anxiety it carries like a ball and chain, has come with a big disclaimer: market trading volumes have been at historical lows as compared to the rest of this last decade, as even institutions have spent considerable time on the sidelines. Most regular investing blokes have spent most of the last few years standing outside the back exit door. So fear-laden is the small investor, that he or she are willing to concede to miniscule bank CD rates rather than suffer the anxiety that might go hand-in-hand with the 12% return on equities. The risk of loss, as we well know, is a much more powerful influencer than the possibility of gain. For most people, the risk premium appears just too great.

Against this backdrop, the professional investor makes his mark. The challenge is getting regular investors to find a way to participate in this environment without having them lose their shirts.

Investor Unprotection, The Three Gorillas, Bollixing Barclays, and Knights Nightmare

With the investors so traumatized, despite the continued rise of the equity markets amidst all sorts of headwinds and setbacks, the vast majority who fled the markets from 2007 through 2009 have not returned, settling instead for earning hundredths of a percentage point of interest on bank or money market fund deposits, and probably for good reason. Lets face it: investors have little reason to trust Wall Street or the regulatory apparatus to protect them from disaster. Despite Dodd-Frank, financial reform continues to be resisted by Republicans and Democrats alike in Congress almost as fervently as by the Wall Street firms being regulated. SIPC the insurance fund designed to protect investors from insolvent brokerage firms -- continues to refuse to compensate victims of two of the industrys failures: Stanford International, and Bernard Madoff. None responsible for the largest financial crisis in the last 100 years have gone to jail. And those concerned about too-big-to-fail after the crisis find institutions to be bigger than ever.

With Wall Street money effectively running K Street and Pennsylvania Avenue in Washington, DC, the small investor simply isnt a big enough player. The original Tea Party activists who actively sought to distance themselves and Congress from Wall Street money are now in bed with those most closely beholden to the financial sector. Meanwhile, the Occupy Wall Street movement, a highly energized effort that had the goal of ripping Wall Streets hands off government institutions, has withered into irrelevancy revealing a mere skeleton of the inflexible, amateurish and anarchist activists whose efforts just happened to resonate with the zeitgeist of a broader population seeking empowerment. Regular investors have been left hanging on a branch, wiggling with the wind.

Meanwhile, the three Gorillas in the room, Europe and the Eurozone, the slowdown in China, and the dysfunction in Congress continue to loudly rattle their cages, although investors have grown increasingly non-reactive. How can that be? European leaders have attempted to kick the can up the road as they piece together and try solutions that make the challenges in the US seem like tic-tac-toe. Yet since the end of 2011, its been clear that Europe has been making real efforts to solve the crisis and limit the devastation. Banks have been propped up, Greece and Spain have gone on austerity diets, and Germany has slowly but increasingly moved to loosen up its purse-strings to assist. Greece may be beyond help, and huge problems continue to confront Spain, Europes fourth largest economy, but the European Central Bank (led by Mario Draghi) seems optimistic that the Eurozone will emerge from their huge debt issues and current recession, and investors concerns have been somewhat pacified. A recent announcement by the ECB to purchase distressed bonds from struggling nations in the Eurozone sends an important message that, short of saving Greece, the other larger nations will be protected. So, in addition to investors worldwide becoming increasingly desensitized to Europes woes, real, albeit slow actions by Europes decision-makers and governments are helping to save the Euro.

China, after the United States, the worlds largest consumer and soon to become the worlds largest economy, has struggled to limit the slowdown in its economy. Not only has it had to deal with an enormous real estate bubble, but the massive slowdown in exports to the floundering developed world and emerging markets has had a profound effect on Chinas purchase of raw materials, agricultural supplies, and yes, US exports. That said, most experts feel that even a slowing Chinas economy is still a massive, growing, consumptive economy, and one which, unlike the US, has a relatively easy time making reasonable economic decisions and seeing them through. The joys of totalitarian rule. The long-term prognosis for China is very promising, however, as the economy slowly benefits from the inevitable rise in domestic consumption that comes along with the ever-growing and consuming middle class.

The US and the Fiscal Cliff. Well speak directly to the US economy in a moment, but for now the political mayhem in DC where terrorism does, in fact, appear to be legal -- is once again taking center stage. Remember the Debt Ceiling Crisis in 2011, when the House Republicans brought about a financial crisis as they nearly collapsed the economy by playing chicken with both a government shutdown and default on Treasury payments? Although it barely averted the first default on interest payments on US Treasury bonds and notes in history, a resulting credit downgrade which dropped the US from AAA to AA, led to a multi-market crash (stocks and bonds) and damaged the economy, while still only kicking the deficit reduction can down the road without rectifying anything.

What is the Fiscal Cliff? First, as a caveat, a reasonable reader might consider taking their pain medication at this time. The term, coined by Federal Reserve Chairman Ben Bernanke refers to what potentially happens at the end of 2012 to substantially reduce the budget deficit: massive slashing of Federal spending (sequestration) along with substantial tax increases via the expiration of the numerous Bush and Obama tax cuts. The Fiscal Cliff, as Bernanke referred to it, will have the effect of massively reducing GDP growth, with the Congressional Budget Office and other economic research entities predicting a probable return to recession coinciding with massive layoffs and increased taxes on the middle class.

Two acts of Congress and subsequent ineptitude have taken us to this place. The Tax Relief, Unemployment Insurance Reauthorization, and Job Creation Act of 2010, signed during the lame duck session of Congress in 2010 sought to extend the Bush era tax cuts for another 2 years in an effort to maintain some economic stimulus and avoid politically difficult decisions during an election cycle. The Budget Control Act of 2011, signed into law in August 2011 came after a near government shutdown by the House Republicans over extending the debt ceiling normally a formality easily discharged by Congress, and ultimately led to the aforementioned credit downgrade, market crash, and downward turn in economic growth. It mandated that a bipartisan commission would come up with a new budget plan that would seek to reduce the large budget deficit and, failing that, force the nation into a dire budget slashing and tax increases that would, hopefully, incentivize a less radical solution.

Well, the bipartisan Joint Select Committee on Deficit Reduction was doomed on formation, as the Republicans hewed to the (Tea) Party line, and refused to include any increase in taxes (via the expiration of the Bush era temporary tax cuts) as part of the solution to reduce the deficit. No compromise was available, despite numerous well-intended efforts by more rational members on both sides of the Committee. After all, the majority of Republicans in the House signed pledges to Radical-in-Chief Grover Norquist to vote against anything that might be construed as a tax increase. And none wanted to incur the wrath of Mr. Norquist or the Party. The thought that one man outside of the elected domain could have such extraordinary control of a huge chunk of Congress is, frankly, stupefying. (Then again, the Citizens United decision is adding still greater pressures in this regard.)

So here we are, three short months away from potential economic and social homicide. While the bet in DC is that Congress will come together and finally agree on something: extending the deadline for a few months. We can only hope that the Congressional members, cognizant of the great damage caused by the government shutdown of 1994 and the debt ceiling crisis of 2010, will give way to compromise. We expect that the can, in expert congressional fashion, will be kicked down the road once again into the next Congress, barely averting disaster. Were also going out on the limb to suggest that a new Congress will give up the Grover Norquist ghost, and begin to make some headway.

Barclays and Knight Capital. If Europe, China, and fanatics in Congress arent enough to give investors hives, Barclays reminded us, only a few short years after the Wall Street-led financial crisis, why the system remains rigged. LIBOR the London Interbank Offered Rate was probably on the vocabulary list of a nerdy few, but suddenly had its fifteen minutes of fame. LIBOR, you see, is the rate charged by banks lending to other banks. That sort of thing would mean nothing to the average Jane, but it just happens to be a rate that is utilized as the benchmark for fixing the rate of adjustable rate mortgages, car and many other loans that consumers and businesses rely on every day. Youd think that, given the critical international import of such a ubiquitous benchmark, and a benchmark that forms the basis of hundreds of billions of dollars of transactions daily, and underpinning over $250 trillion in financial derivatives, that every effort would be made to insure that this rate was properly set, free from manipulation and perversion.

No such luck. It turns out that Barclays had been misrepresenting their rates for some time, with banks profiting massively from the manipulation by lending at higher interest rates than they were reporting and enjoying greater profit spreads as a result. Traders in the banks, aware of these manipulations, were able to exploit sudden manipulated changes in interest rates to generate massive profits in derivatives trades. Moreover, it turns out that regulators have either suspected or known for some time that this sort of behavior had been going on, and largely turned a blind eye. Indeed, it appears that this behavior has been common practice for at least twenty years, going back at least to 1991.

If that wasnt enough to spook the bejesus out of investors, even professional ones, Knight Capital did its level best to do just that. Knight Capital, you see, is one of the very largest trading and market making firms on the New York Stock Exchange, and one that engages in high-frequency trading essentially the use of automated, computer driven trading strategies that emerge, not from the brains and mouths of human traders, but rather, in I Robot-like fashion, from computers infallibly trading stocks at incomprehensibly fast speeds, bypassing any chance for human error.

So they say or said. On August 1, Knights trading robots went rogue, trading hundreds of millions of dollars of stocks at tremendous losses, roiling markets. Knight, however, suffered the biggest loss, as the value of their stock fell nearly 75% in the aftermath. The issue would have been less of a distraction had it not been for the infamous Flash Crash of 2010, when faulty high frequency trading algorithms caused nearly a 10% decline in equity stocks in just minutes. The fact is that many day-to-day trades are driven by these new technologies. Over the long term, stock prices more or less continue to reflect the potential earnings of their businesses. Still, the failures of Knight Capital and the Flash Crash before it have once again sent investors to the exits, with billions leaving the markets just over the last few months.

Jamie and The Whale. Back early in May, Jamie Dimon, the CEO of the Wall Street megafirm, JP Morgan, announced a trading loss in the London office of $2 billion. Much like a defense contract, however, by June that amount had shown losses that ballooned as high as $9 billion. It turns out a Mr. Iksil, a London trader at the firm, made a whale of a bad bet involving complex derivatives as hedges. Apparently while his immediate superiors had some knowledge of the trades, New York central did not. So what turned out to be a trade that was intended to be protected from significant downside risk, turned into something far worse, jarring the markets, the stock price and the credibility of Wall Streets premier firm and shining star, Jamie Dimon. With headlines about the debacle making leading even mainstream news as the markets jerked once again, Dimon was dragged through Congressional hearings, and investors, once again, were stunned that anything so large could happen under the wings of such a respected Wall Street firm. Déjà vu, as Yogi Berra so aptly put it, once again.

Jamie and The Whale. Back early in May, Jamie Dimon, the CEO of the Wall Street megafirm, JP Morgan, announced a trading loss in the London office of $2 billion. Much like a defense contract, however, by June that amount had shown losses that ballooned as high as $9 billion. It turns out a Mr. Iksil, a London trader at the firm, made a whale of a bad bet involving complex derivatives as hedges. Apparently while his immediate superiors had some knowledge of the trades, New York central did not. So what turned out to be a trade that was intended to be protected from significant downside risk, turned into something far worse, jarring the markets, the stock price and the credibility of Wall Streets premier firm and shining star, Jamie Dimon. With headlines about the debacle making leading even mainstream news as the markets jerked once again, Dimon was dragged through Congressional hearings, and investors, once again, were stunned that anything so large could happen under the wings of such a respected Wall Street firm. Déjà vu, as Yogi Berra so aptly put it, once again.

Investors, therefore, have every reason to feel that the game is either rigged, unsupervised, and/or capable of massive chaos due to things well out of their control. Even still, it remains remarkable that Congress remains reluctant to improve regulation and properly fund those in charge of oversight and keeping the markets sane and at least reasonably fair. Remarkable until one is reminded of the intimate relationship between the key Congressional members and Wall Street contributors.

Strengths, Weaknesses, Threats

Overall economic growth continues at a relatively slow pace, and with second quarter GDP growth revised downward to 1.3%, significantly slower than the 2.5% that was predicted by most at the end of 2011. Third quarter growth shows but a small anemic improvement, at a projection of 1.7%. The slow growth crawl, particularly given such a high unemployment rate has left many consumers with a slightly improving, but still dismal outlook that belies improvements across several areas. Business is less optimistic. Retail sales, durable goods orders have generally been improving over the year, although durable goods orders dropped significantly in August due to a drop in airlines orders. Personal income is also up slightly. Corporate profits remain strong, however, and earnings continue positive, with over 70% of corporations beating estimates, although projections going forward are less sanguine. Corporate sales revenues have improved now for 11 straight quarters, and corporations are holding record levels of disposable cash cash that, when appropriate, can be reinvested in capital purchases and additional hiring. With retail and industrial sales growing ever so slightly, and exports solid, the earnings picture seems more positive than negative.

The job situation so central to the mood in America remains improving ever-so-slightly, but still uncertain. Grave concern about the unemployment level, in fact, was the phrase used by Ben Bernanke to justify the latest Fed actions. The fact is that we have recovered nearly one-half of the jobs lost during the financial crisis and recession. Private sector job growth, unsettlingly significantly below 100,000 per month from April to June of this year, appears to be heading back up to the 100,000 per month area, although government jobs continue to be under tremendous stress due to continuing budget cuts on the state and local levels. Accordingly, the unemployment rate needle seems to be stuck around 8.3%, and U6, the Underemployment number those employed part-time, for example instead of full-time -- remains in the near-brutal 15% range. Monthly jobless claims remain high nearly 380,000 -- and seem to be bouncing around that number mostly all year.

Until businesses feel more optimistic and start hiring more aggressively, and until banks loosen the credit strings still further for small and medium size businesses, job growth is likely to continue at this slow rate for one or two more quarters at least. This assumes, of course, that we dont drop off the Fiscal Cliff causing massive government cuts and payroll tax increases on one extreme, or the passage of Obamas American Jobs Act, which could add massive job numbers on the other. So despite the uncertainty in Congress which darkens the overall environment, the fact remains that the labor markets seem to be both stabilizing and improving ever so slightly.

Housing, however, may be the real shining star. For nearly four years, the beleaguered housing market has been both a drag on GDP and a real source of continuing unemployment. For nearly three years, we have been looking for strong data to support the improvement of this critical sector. However slow in coming, the latest home sales numbers, prices, and permit numbers have finally been on the rise. The recent Case-Shiller index demonstrates their three indexes showing positive for the first time since 2010. Should housing growth continue, a substantial boost will be injected into the economy. The recent actions by the Fed should only help, although it will take some time before the banks are able to ratchet up the capacity to process new mortgage applications. Lest investors become too upbeat, keep in mind that the banks have been exceedingly slow to avail themselves of cheap credit over the last few years, and the concern remains that banks will sell their bad mortgages to the Fed while hoarding cash instead of lending.

Interest rates and inflation remain low. Low interest rates allow for less expensive borrowing for homeowners and businesses alike, allowing opportunities to both reduce debt and consume, and rates are still hovering at the lowest levels in a century. The downside of such low rates is felt most acutely by fixed income investors, particularly the elderly relying on income from bank account CDs, secure bonds and the like.

Inflation remains extremely low at 1.7% over the year, having ticked up a tad, thanks to rising gasoline prices and agricultural grains, the latter largely due to the drought (certainly not due to climate change according to most experts in the House of Representatives) -- which has devastated the Midwest. Although grain prices have risen dramatically, the impacts on food prices here have been so far minimal, largely due to the fact that the cost of grain represents a small component of the price of cereals, pastas and other finished food products. (Poorer third world economies will take the biggest hit due to these rising grain prices.) Moreover, oil and gas prices are still at very favorable levels, with natural gas downright cheap. Commodity prices remain neutral, still significantly lower than a few years ago. Low inflation also means that income is not being significantly eroded by rising prices.

Thats the good news. But weaknesses, in addition to the ongoing negative impacts of Europes recession and Chinas slowdown, remain real. With consumer and business sentiment low, and conflagration in Congress ever-present, a bit of a self-fulfilling prophecy is taking place. Uncertainty, a term used ad-infinitum by business groups to describe the sentiment of the domestic business community, is the rationale thats being spun to explain the lack of hiring, while squeezing the last drop of productivity from an overworked, overstressed workforce, or at least what little of it remains after outsourcing. Many feel this to be negative self-talk, a by-product of the fear generated by right wing, pro-business, anti-government instincts and parroted by the mainstream and financial media. In addition, concerned about further Congressional brinkmanship over fiscal policy that might turn the economy back to recession, the unknown impacts of impending socialist healthcare reform, and an uncertain global economy, many businesses are reluctant to throw their hats into the ring. So despite corporate cash and profits at near record levels, a pro-Wall Street (republican and democratic) Congress and President, businesses sit on the sidelines, and instead of investing are, in many cases, using that cash to donate to their candidate of choice.

Having shown a downturn in sentiment over the summer, manufacturing has made a strong comeback in September, showing a significant expansion for the first time in several months. While output deteriorated in late summer, new orders substantially increased in September, surprising many economists. While the slowing global economy is certainly asserting its impact, at the top of the list of concerns expressed by manufacturers is not the very real recession in Europe, but the deteriorating political climate. Whats also interesting is that while manufacturing output has grown 20% since 2009, manufacturing wages have grown a scant 4% during that same time. Companies are doing more with fewer employees, and paying them less. As some of the uncertainties i.e. the Fiscal Cliff, healthcare, the elections work their way through, a more objective consensus may begin to emerge. As of now, the situation remains murky. If manufacturing manages to continue expansion despite the political uncertainty and European recession, a significant increase in hiring could be in the works, and that would be extraordinarily welcome news.

Threats continue as well. According the Pew Center, over $3 trillion in unfunded pension liabilities exist mostly amongst the state and local municipal workers across America, and not including another $1 trillion in estimated unfunded healthcare costs. Coming at a time when municipalities can least afford making any payments into these funds, the actuarial assumptions based on pipe-dream investment returns of 8% and the losses sustained from 2007 through early 2009 are leaving accounts just a tad (shall we say) short. So when even normal contributions would be challenging, some municipalities are having to contribute 2 or 3 times their normal levels. The additional stress being placed on municipalities on top of drastically reduced tax revenues is extreme. Its remarkable, frankly, that far more municipalities havent already gone into bankruptcy. Many yet may, or be thrown into acute austerity and additional rounds of public layoffs.

Geopolitical events, much harder to predict, are also worthy of consideration. While Iran and a possible impending attack on their nuclear ambitions receded in likelihood over the last six months, only recently has Israel ramped up, again, its saber-rattling. Should that escalate further into an actual strike, the impacts on oil prices would be substantial, despite the fact that weve reduced our reliance on foreign oil. Syria, meanwhile, while a bit player on the world stage, could impact the system should US or international military action intercede, and escalate tensions throughout the Middle East, as well as between US and Russia, Syrias ally. Events over the last few weeks have been sobering reminders about how little is really predictable about events that can befall this area of the world.

Oil prices currently are trading roughly near where they began a year ago. Certainly, gasoline prices have crept up the last several months, but overall energy costs remain fairly stable. Importantly, however, natural gas prices, currently trading at almost 50% lower than the already low levels a year ago, and increasingly an essential source of energy for utilities and manufacturing, is a very significant positive. While an invasion of Iran or other geopolitical flare-up could see a rapid rise in oil prices, we again see these as short lived. So while this remains a threat, modest energy prices by and large remain a strength, and all of the concerns are largely old news, and baked into the market prices.

Eurozone. The biggest known threat, however, emanates from Europe. Should the Eurozone fail to come to an accord that works to stabilize Spain and Italy, and minimizes the impact of what seems now to be an all-but-inevitable Greek default and departure from the Euro, the shocks here could be very considerable. A series of major bank failures as a result of government defaults or deterioration of credit quality could initiate a domino effect of bank insolvencies that could easily spread across the Atlantic. While its not likely to lead to a replay of 2008, the damage still could be considerable, and further destabilize already fragile financial markets.

Many investors, however, have been concerned that a complete collapse of the Euro is impending and will lead to economic catastrophe. We just dont see that happening. It has become increasingly obvious that the Eurozone powers that be will continue to work to solve the complex issues as leaders and officials have made clear. Although it will take a considerable amount of time perhaps years to work through the complexity and number of the problematic issues -- governments, politics, costs, bank logistics, etc. -- the Eurozone will likely emerge strong, despite the current recession some of Europe is currently experiencing. So while problems in Europe remain a threat and will continue to be so for some time, the threat is better known, and the problems and solutions better understood by investors, central bankers, and the elected officials of the Eurozone nations.

The Fiscal Cliff. We see the Feds drawing a line in the sand as important in drawing attention in Congress and the American public to looking past a Tea Party-driven focus on dismantling government and reducing taxes, to seeking a more balanced approach to both stimulating growth and seeking long term deficit reductions. While an obstructionist House could, once again, obstruct and/or blow up budget discussions leading to another damaging credit downgrade, we see this as increasingly unlikely. Tea-Party House members gave their party a black eye after the last budget debate with the Party elders finally intervening to prevent another debacle. No doubt the House Republicans will be looking to the mid-term elections in 2014, hoping not to provide fodder for a Democratic rout. We expect, as weve seen in Europe, a dance unfolding which combines kicking the can down the road, with modest agreements which demonstrate positive progress over the next six months. So while this remains a threat, we feel it less an issue now.

The Elections and the Affordable Care Act. Some pundits have argued that an Obama reelection combined with Democratic retention of the Senate would present a threat to the economy. We disagree. Historically, not only have election year markets been positive, theyve been positive even when a Democrat is leading in reelection prospects. Moreover, while Wall Street and the business-friendly US Chamber of Commerce may see Mitt Romney as a dream candidate, its hard to imagine a President thats been more friendly to Wall Street and the business community than Mr. Obama. Treasury Secretary Timothy Geitner has had the back of Wall Street since the crisis unfolded in 2007. No threat here.

The Affordable Care Act aka Obamacare -- seen as potentially leading to the demise of the Nation and life as we know it has had little, if any negative impact, since the Supreme Court shockingly ruled in June in support of the legislation. Health care costs rose far less than usual over the past year, and while businesses are wrestling with some of the needed changes in 2014 when some of the mandates of the legislation are triggered, the impacts are being seen, ultimately, as relatively benign in 2013. While there will be winners and losers in different areas of the healthcare industry, those impacts are not seen as being extreme one way or the other. So, while this issue and particularly the uncertainty around it may have added to the roiling of markets earlier this year, the threat is effectively done and gone for the next six months or more.

The Markets Looking Ahead

Even with the continued market rally, the S&P500 is still reasonably, if not cheaply priced. While earnings growth going forward may slow somewhat, they are growing, and with both the US and the global economy growing, with major headwinds increasingly understood, we cant see why stock prices shouldnt rise over the next year. A market pull-back or even a correction triggered by some event might be expected given the run-up thus far, and should stock prices continue to move upward quickly, or sustain the current increase for several more months, this is more likely still. An invasion of Iran, massive Mideast upheaval, or European nation or bank failure could wreak havoc to stock prices and investor confidence, but we feel that as damaging as these events could be in the short term, long term economic devastation is highly unlikely.

Regular Equity investors, meanwhile, have continued to remain largely on the sidelines or in fixed income securities, not only because of the trauma of 2007-2009, but also the constant barrage of negative news from the media. However, with yields remaining puny in low-risk Treasuries and CDs (10 year Treasuries are currently yielding a miniscule 1.6%), large dividend paying companies are becoming increasingly attractive to even the more conservative investors, many in fear of outliving their assets. Moreover, even though the economy may be limping along and consumer confidence far from upbeat, stocks continue to march forward up the wall of worry as discussed earlier.

Increasingly, we expect investors to recognize this trend, which will bode even better for stock prices. And as interest rates for intermediate term and long term fixed income securities continue ticking up, and with those investors seeing their account values beginning to drop, this trend is likely to intensify, as investors seek out dividend paying equities as alternatives to bonds that might be declining in value on paper. The fact of the matter is that investors are invested at historical levels in bonds, fixed income mutual funds and ETFs, and money market funds. When those prices start to deteriorate, many of the exit doors are likely to lead to historically conservative dividend paying stocks. Moreover, with so many investors on the sidelines in money market funds and the like, when they do capitulate as the move into equities finally goes mainstream, the upward pressure on stocks could be very significant. Should a budget deal take place, housing prices continue on the upswing or other tailwinds provide a boost to investor sentiment, the rush in to equities could be swift, indeed.

As weve been indicating for some time, for Fixed Income investors, the yellow caution light is flashing brightly. We have long argued that investors in intermediate and long term fixed income securities needed to be mindful of even modest interest rate increases, as these would erode asset values. Long term treasuries, for example, have seen drops of nearly 10% from their July highs. And even high quality intermediate bonds, currently offering yields just over 3% had seen values drop 2% or more during much of that same period. While most of our investors have significant positions in fixed income investments, we diversify those positions extensively as we seek to provide income in this difficult interest environment but remain very vigilant regarding interest rate changes.

With the likelihood of massive market disruption decreasing over the last six months, most of our clients have been returned to their target portfolios. We remain reluctant, however, for all but the most risk tolerant investors or investors with very long time frames in mind, to remain overly positioned in equities. While we feel that the argument for equities is improving, and we are continuing to increase positions in those asset classes, conservative clients who are unable to comfortably sustain drops in asset values of 10% or more should remain highly diversified. As discussed at length above, market volatility can leap rapidly as computers react instantaneously and en masse to events, non-events, or worse, programming glitches. Hence: cautious optimism, with vigilance. The arguments in favor of careful asset management remain strong.

Wishing all a Wonderful, Colorful, and Happy Autumn.

In Peace,

Ron Stein, CFP

Good Harvest Financial Group

631.423.6501

rstein@goodharv.com